SMM November 29:

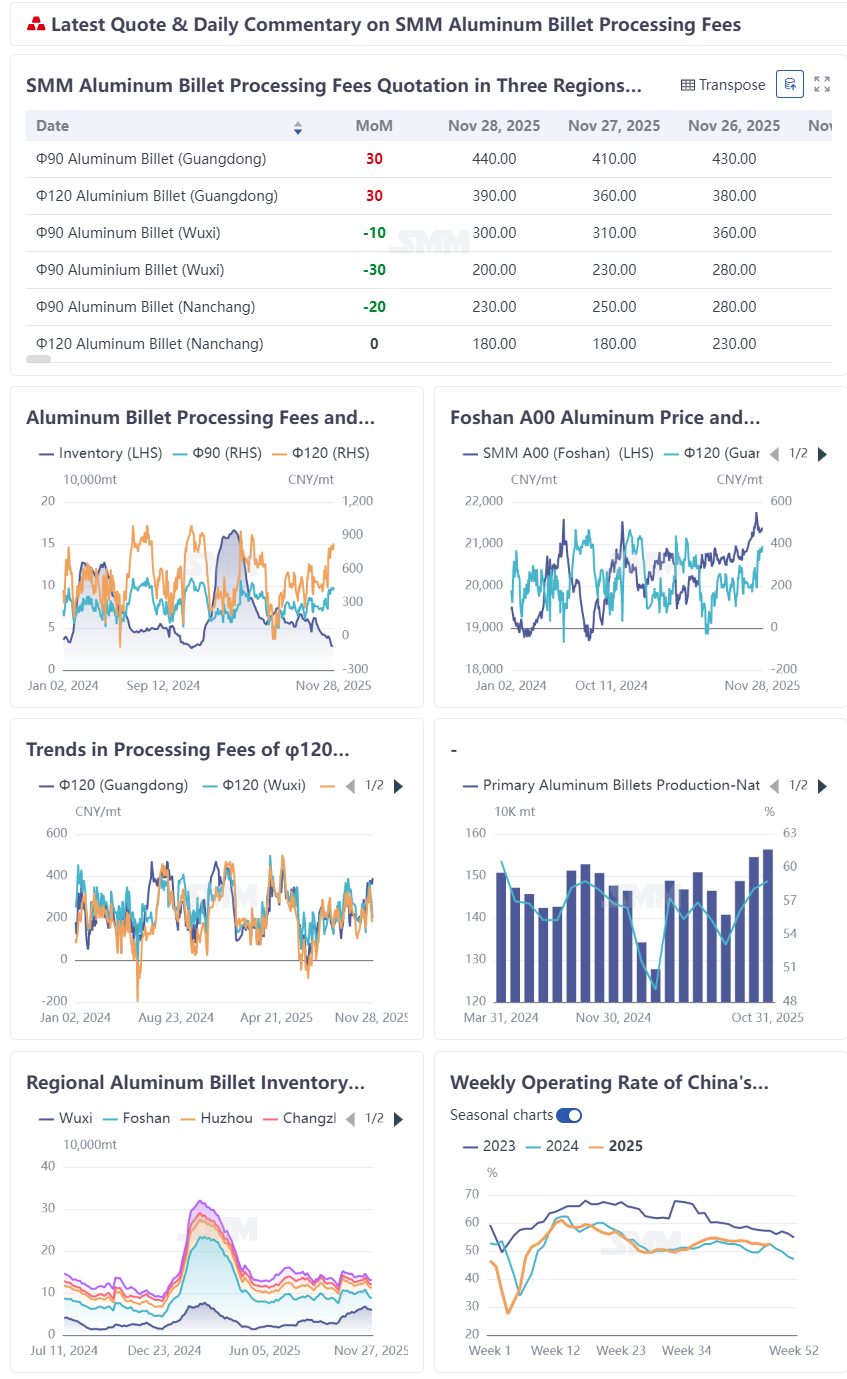

As of November 28, the processing fees of φ120 aluminum billets in South China (centered in Foshan) were quoted at 390 yuan/mt, while those of φ90 aluminum billets reached 440 yuan/mt, having risen by over 200 yuan/mt from the monthly low and approaching the annual highs of 470 and 520 yuan/mt recorded in 2025. Although prices fluctuated in Wuxi and Nanchang, they also showed significant recovery from mid-month lows. The strong performance in late November appeared to be a short-term pulse driven by the pullback in aluminum prices and concentrated restocking, but in reality, it was an inevitable outcome of the seasonal pattern in the aluminum billet market in November—short-term price pullbacks were merely a "catalyst," while the annual demand pace provided the core support.

I. Seasonal Pattern Drives: Processing Fees Historically Show Significant Upside Probability in November During Peak-Off Season Transition

Historical data indicates that November often serves as a seasonal window for rising aluminum billet processing fees, with a recurring supply-demand mismatch during the transition between peak and off-seasons. After aluminum prices surged to their H2 peak and then pulled back rapidly, year-end rush-to-complete-work demand led to a stronger-than-usual off-season. As the market transitioned into the off-season, aluminum billet supply marginally declined, while traders actively entered the market to capitalize on opportunities. Downstream users restocked on price dips and engaged in essential stockpiling, with inventory declines in both sectors creating positive feedback. Taking the average price of Φ120 aluminum billets in Foshan as an example, processing fees continued to strengthen after the September-October peak season for three consecutive years from 2023 to 2025. Particularly in November 2025, domestic aluminum billet processing fees exhibited an unexpectedly strong regional divergence. Against the backdrop of an annual average price of Φ120 aluminum billets in three regions projected to be only slightly over 200, the robust rise in November aluminum billet processing fees, supported by firm pricing, was especially noteworthy.

II. Support from Supply and Inventory Side: Social and In-Factory Inventory Both in Destocking, Spot Aluminum Billet Supply Tightens

Supply side, in early November, persistently high SHFE aluminum prices suppressed some downstream demand, weakening downstream orders gradually transmitted to upstream aluminum billet producers, processing fees are expected to remain under pressure, some enterprises already have marginal production cut plans, aluminum billet production in various provinces is expected to decline to varying degrees in November. According to SMM statistics, domestic daily average production of primary aluminum billets in October held steady at around 51,000 mt/day MoM from September, and is expected to drop back slightly to 50,000 mt/day in November, showing a marginal contraction trend.

In November, an aluminum billet enterprise in south China reduced its aluminum billet production by approximately one-third due to a shift in production to aluminum busbars. This was primarily attributed to the overall weak market conditions and low profitability of aluminum billets throughout the year. The company subsequently shifted its focus to other non-ferrous metal businesses and is expected to maintain the reduced production level for aluminum billets in December. This also contributed significantly to the relatively strong trend in aluminum billet processing fees in south China during November.

Social inventory side, according to SMM statistics, domestic aluminum billet inventory in mainstream consumption areas stood at 131,000 mt on November 27, down 6,500 mt WoW from last Thursday, maintaining an overall destocking trend for six consecutive weeks; after aluminum prices retreated from highs in the recent week, warehouse withdrawals showed positive feedback first, aluminum billet warehouse withdrawals reached 53,300 mt during 11.17-11.23, up 5,700 mt WoW, a 13% increase WoW, and at a high level for the same period in recent three years.

In-factory inventory side, according to SMM survey statistics, domestic aluminum billet in-factory inventory in late November was about 100,000 mt, down 21,000 mt MoM from the same period last month, and down 61,000 mt from after the National Day holiday, a decrease of nearly 40%; average days of inventories fell 0.8 day MoM to 2.0 days, and dropped 1.4 days from after the holiday.

Relative restraint on the supply side accelerated destocking of both social and in-factory inventories, spot aluminum billet circulation tightened further, providing additional support for upside room in processing fees in late November.

III. Demand-Side Support: In South China, large and medium-sized construction aluminum extrusion enterprises maintained stable production, while industrial extrusion orders from automotive and 3C sectors provided a dual-engine boost.

In October, the operating rate of China’s construction aluminum extrusion industry was 40.4%, basically flat MoM. Some large extrusion enterprises in Guangdong reported that construction extrusion still accounted for roughly 80% of their output; production pace remained steady but lacked growth momentum.

October’s operating rate for industrial aluminum extrusion stood at 53.9%, down 1.3 ppts MoM, mainly because PV extrusion came under pressure.

Entering November, with building-material output holding steady, the automotive sector—core downstream for industrial extrusion—continued its high-growth trajectory in 2025. November output was projected to exceed 3.4 million units, likely setting new highs for both the year and the past four years. Driven by the lightweighting trend, aluminum extrusion demand rose inelastically; automotive extrusion performed steadily better throughout the year. In particular, automakers’ year-end push for annual targets boosted parts orders, pulling aluminum billet procurement. Market feedback showed that mid- to high-end branded aluminum billets for industrial extrusion traded noticeably stronger recently.

Meanwhile, the “Double 11” and “Double 12” e-commerce promotions and a flurry of year-end consumer-electronics launches led to a short-term concentrated release of 3C extrusion orders, further lifting aluminum billet processing demand.

On the PV side, a leading PV frame producer in Anhui noted that recent export orders performed well, effectively offsetting reduced orders from domestic module makers and supporting operating rates.

This week, China’s aluminum extrusion industry operating rate came in at 52.5%, up 0.4 ppts WoW, halting the decline and stabilizing—providing some confidence to the aluminum billet market.

IV. Regional Divergence: Guangdong-Shanghai Price Spread Maintained Triple Digits, Spot-Futures Price Spread Strengthened Suppliers' Confidence to Hold Prices Firm in South China

By mid-week, φ120 aluminum billets in east China (Wuxi, Nanchang) pulled back to around 200 yuan/mt, while Foshan remained relatively firm, supported by a Guangdong-Shanghai price spread exceeding 100 yuan/mt. Driven by regional price differences, earlier supplies from north China were mostly directed to east China, leading to relatively ample circulating supply in the east, with in-transit volumes still trending upward. South China currently relies mainly on supplies from south-west China, and new capacity in Guangxi and other regions has not yet ramped up significantly, resulting in a slight shortage of mid- to high-end branded supply, which bolstered suppliers' confidence to hold prices firm in the south. As of November 29, the SMM Spot Procurement Sentiment Index for primary aluminum billets in south China was 3.17, while the Sales Sentiment Index reached 3.78, both hitting new highs for H2.

V. Short-Term Contingent Factors Overlap: Aluminum Price Correction to Near Monthly Average Stimulates Restocking Demand, Leading to Phased Rapid Release of Demand

The aluminum price had held up well for nearly half a year. In mid-to-late November, SHFE aluminum pulled back from a nearly three-year high above 22,000 to near the monthly average. Downstream extrusion enterprises, which had been holding cash and waiting on the sidelines due to high aluminum prices, phased in rigid restocking demand. Moreover, the medium and long-term bullish logic for aluminum remained unchanged, with downstream bullish sentiment dominating. Traders actively entered the market to purchase and make markets, while suppliers' sentiment to hold prices firm intensified, directly driving a short-term rapid rise in processing fees. Short-term restocking amplified demand elasticity, providing support for the surge in processing fees. However, caution is warranted regarding the risk of restocking demand receding after aluminum prices stabilize and rebound.

Conclusion: The Surge in Aluminum Billet Processing Fees in November Represents an Accidental Acceleration Within an Inevitable Trend

Overall, the strengthening of processing fees in November was an inevitable result of the combined effects of seasonal patterns, demand resilience, and regional supply-demand mismatch. The concentrated restocking triggered by the aluminum price correction was a contingent factor but served as the main driver for the short-term rapid rise in processing fees. SMM believes that as the traditional off-season arrives in December, the probability of seasonal weakening in downstream demand increases. Meanwhile, as aluminum billet enterprises' production willingness enters a positive cycle, coupled with the difficulty of a significant pullback in the proportion of liquid aluminum converted to billets, the upside room for aluminum billet processing fees will be constrained after supply-demand repair. Fluctuating at highs under pressure is expected to be the main theme by the end of 2025.